Please click here to access part I of this blog post.

Market Barriers

China’s growing import of iron ore and coking coal from abroad has resulted in a predicament of overreliance on a few key exporters, Australia, Brazil, and India, and has recently produced investments in other regions. A setback in iron ore or coke imports due to international issues could force China’s iron and steel industry to rely on less efficient domestic supplies in its steel production, resulting in higher greenhouse gas emissions. Furthermore, lack of open firm, local, and provincial level technical data on energy use for the public makes it more difficult for foreign companies to perform accurate analysis of China’s iron and steel market. As a result, possible foreign joint ventures are at a disadvantage in contrast to state-led investment which has better access to this information.

Financial Barriers

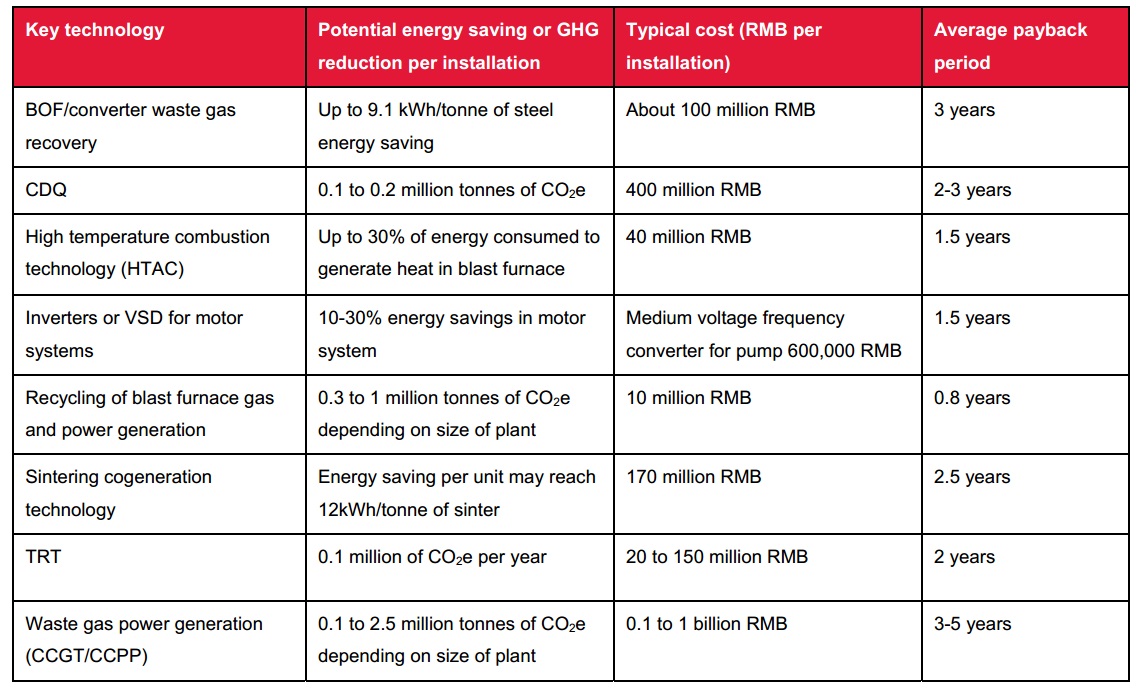

Among smaller iron and steel producers with fewer financial resources, short investment payback thresholds, risk, and limited access to capital could prevent possible investment planning. However, among larger iron and steel firms, many greenhouse gas emission reductions technologies are available with payback periods of less than five years (as seen in the following chart).

Recommendations

Adopt Scrap Steel Collection Programs and EAF Subsidies: Local and national programs which incentivize the collection and recycling of scrap steel within China can increase the relative profitability of EAF compared to BOF. Further adoption of EAF through project subsidization can produce a new market in China as EAF plants are less capital intensive, take less time to build, and can be more responsive to demand than BOF plants due to EAF’s flexible production cycles.

Create Domestic Energy Efficiency Programs: Chinese adoption of an energy efficiency program which assists the iron and steel industry in energy efficient management, evaluating performance, and electricity demand forecasting can help smaller sized steel plants plan and carry out energy efficient upgrades with private capital. Alongside China’s developing cap and trade programs, this could help the iron and steel industry eventually produce a price of carbon within China.

Expand the Availability of Emissions Data: Access to emissions data on the firm, local, and provincial levels can help foreign firms join Chinese firms in choosing partners for appropriate projects. Currently, only 25% to 30% of Chinese steel firms are members in the World Steel Association, and 70% are members of the China Iron and Steel Association – both organizations geared towards providing private inside information between firms.

Develop Local Natural Gas Resources: Iron reduction can be done through natural gas instead of coke through Direct Reduced Iron furnace technology. While China’s natural gas resources are more limited than those in the United States due to geographical and technological constraints, this could still result in lower GHG emissions per ton of steel.

Engage in Multilateral and Bilateral Technology Programs: China should maintain and expand its current participation in technical assistance programs. Japan’s assistance through the JICA Energy Efficiency Training program, Green Aid Plan End-Use Energy Efficiency Program, and the Asian Development Bank’s Shandong Energy Efficiency and Emissions Reduction Project have proven that China can transform foreign aid into iron and steel emissions reduction projects while maintaining current levels of employment and stability. Additionally, dialogues such as the U.S. – China Strategic and Economic Dialogue and the ASEAN+3 meetings can promote cooperation on developing energy efficient iron and steel technologies between China and other actors.

We look forward to uploading our final China paper, which will give a more in depth analysis of China’s iron and steel industry emissions and abatement strategies. Please feel free to refer to our country reports when released and provide feedback for future research after this project has ended.

Leave a Reply